2024 Venture Capital in Africa Report

Download the report

Key Findings

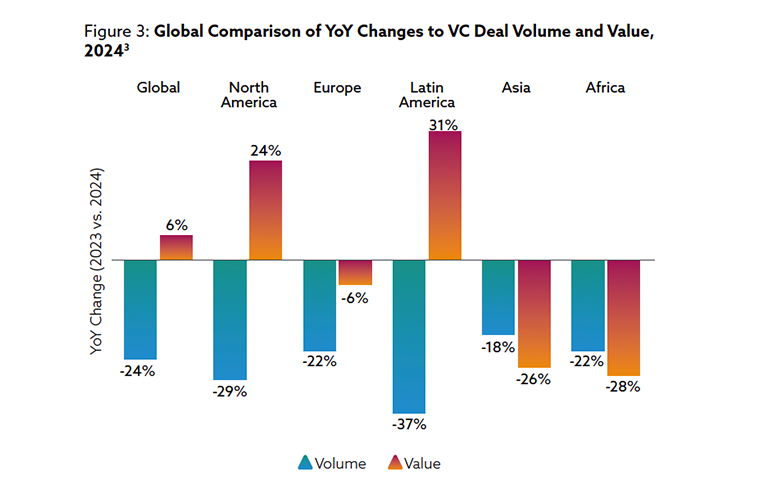

Africa in the Global Context

In 2024, Africa's venture ecosystem faced a 22% drop in deal volume and a 28% decline in deal value. This pronounced downturn came approximately one year after global markets, highlighting a delayed but significant adjustment. While global venture funding saw modest recovery with a 6% increase in deal value, Africa's sharper contraction placed it at the opposite end of the growth spectrum compared to other regions.

Despite these contractions, African startups demonstrated remarkable competitiveness at later funding stages. At Series B and Series C rounds, African ventures secured median deals of US$29mn and US$38mn, respectively, surpassing global averages of US$21mn for Series B and US$35mn for Series C. This underscores that while Africa's early-stage funding faced significant headwinds, companies securing growth capital achieved substantial success on the global stage.

The Venture Landscape in Africa

Deal Volume and Value

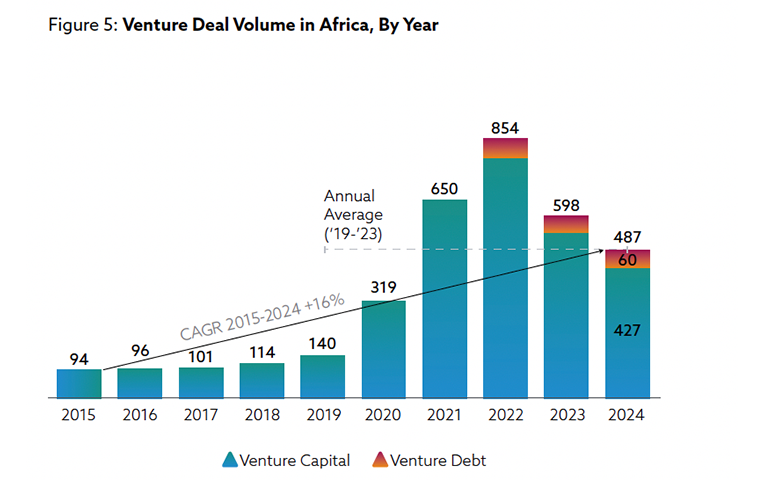

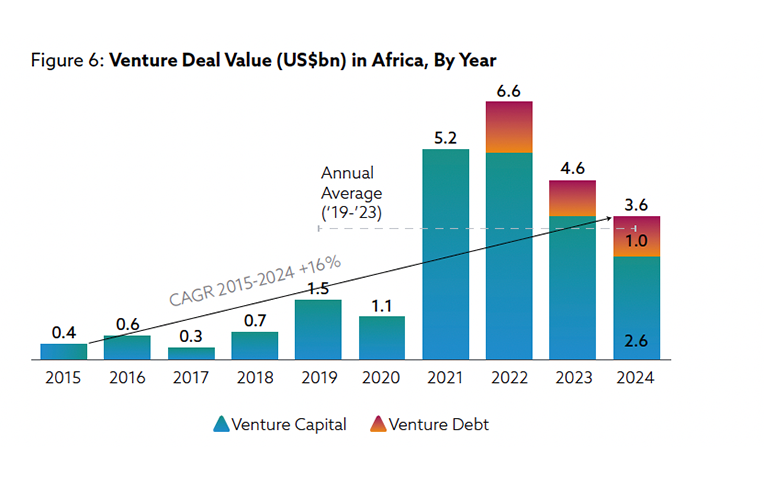

Africa's entrepreneurial ecosystem collectively secured 487 deals in 2024. This was distributed as 427 venture capital deals with a value of US$2.6bn and 60 venture debt deals worth US$1bn.

Despite declining activity, the median VC deal size rose to US$2.5mn (+32% YoY), indicating higher deal values despite a drop in overall activity.

Deal Profile by Investment Stage

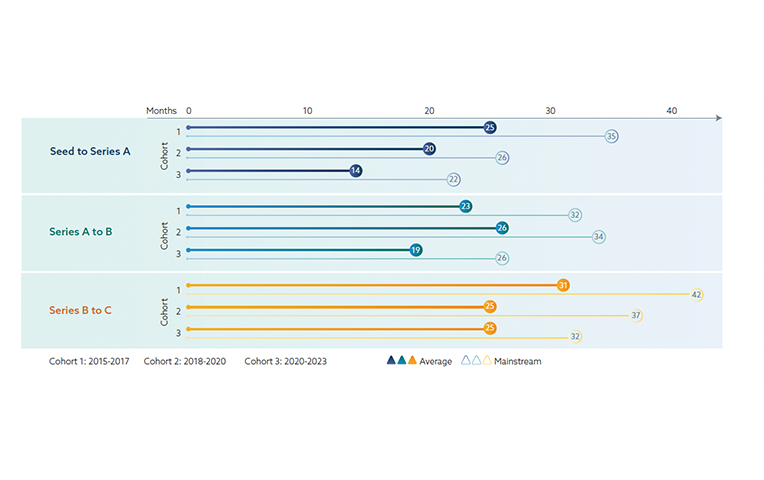

Funding was concentrated at two ends: early-stage and mature ventures, whilst mid-stage companies faced heightened pressure. Funding rounds progressed more quickly, with Seed to Series A averaging 14 months, Series A to B at 19 months, and Series B to C at 25 months, reflecting increased efficiency in follow-on funding.

This bifurcation in the market is evident in the rising median deal values at both ends of the spectrum. Seed stage median values increased from US$1.2mn in 2023 to US$1.5mn in 2024, while Late Stage medians rose from US$75mn to US$100mn over the same period. Companies in the Early Stage bracket found themselves in a particularly challenging environment, with investors showing clearer preference for either early validation or proven maturity.

Deal Profile by Geography

West Africa maintained its lead in deal volume for the fourth consecutive year, driven by Nigeria, which was the most active country by volume at 16% of deals. Despite lower volumes, multi-region deals garnered the highest total capital, while the 'Big 4' (Nigeria, Egypt, Kenya and South Africa) collectively represented 55% of all deals and 64% of capital.

Multi-Region deals ranked first in Africa by deal value. Notably, multi-region startups are shifting from pan-African expansion strategies to broader emerging market playbooks, using later-stage funding to scale into regions like Southeast Asia, Latin America, and beyond.

Exits

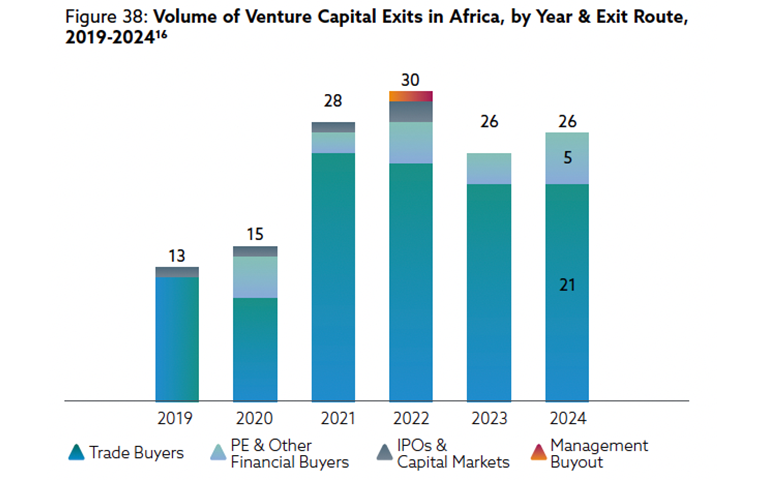

Venture-backed exits in Africa are gaining momentum, with 138 recorded between 2019 and 2024—reflecting a clear upward trend over time, despite remaining flat in 2024. Trade sales continued to dominate, accounting for 84% of all exits that year, with an average holding period of 3.8 years.

Fundraising

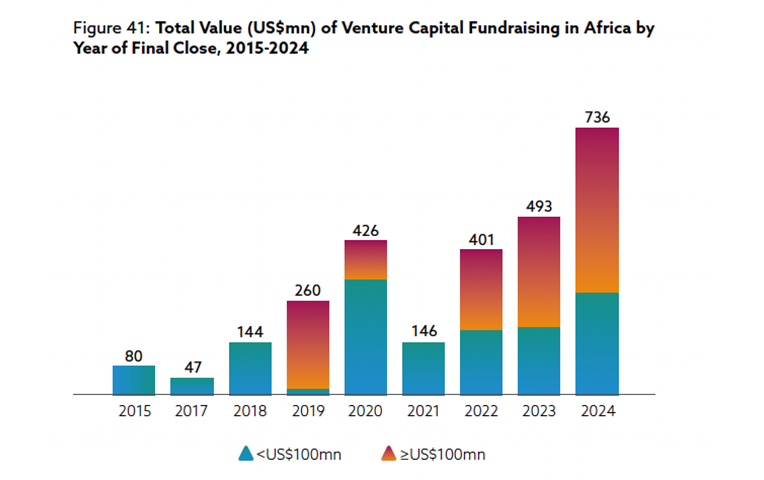

US$2.7bn in capital commitments was raised by 35 unique fund managers across 41 funds between 2015 and 2024. A 25% CAGR over the period underscores the positive, long-term growth of Africa’s VC ecosystem. In 2024 specifically, 20 funds secured US$879mn, including interim closes.

Technology and Innovation

Financials was the most active sector by volume (30%) and attracted the largest share of capital (59%) in 2024. Reflecting this dominance, FinTech and Digital Banks led tech-enabled deal activity, with 116 deals that collectively raised US$1.4bn.

Clean & ClimateTech gained ground in 2024, doubling its share of tech-enabled deal volume to 13%. Meanwhile, AI broke into the top four most funded verticals with 42 deals cumulatively valued at US$108mn.

Investor Profile

614 active investors participated in African VC in 2024, representing a 21% decrease from 774 in 2023. However, local investors took the lead for the first time, with African investors forming the single largest group (31%) of active VC participants on the continent.